Insights

From Maquiladoras to Microchips: Expanding Mexico’s Semiconductor Manufacturing

In times of mounting global uncertainty around tariffs and possible challenges of nearshoring, investment in the growth and consolidation of semiconductor manufacturing may prove essential to Mexico’s long-term growth. Global semiconductor sales totaled US$627 billion in 2024 and are projected to exceed US$1 trillion by 2030, according to an industry outlook from Deloitte. As outlined in a previous Milken Institute report, Mexico is well-positioned to emerge as a major semiconductor producer by leveraging its geographic advantages and established manufacturing base.

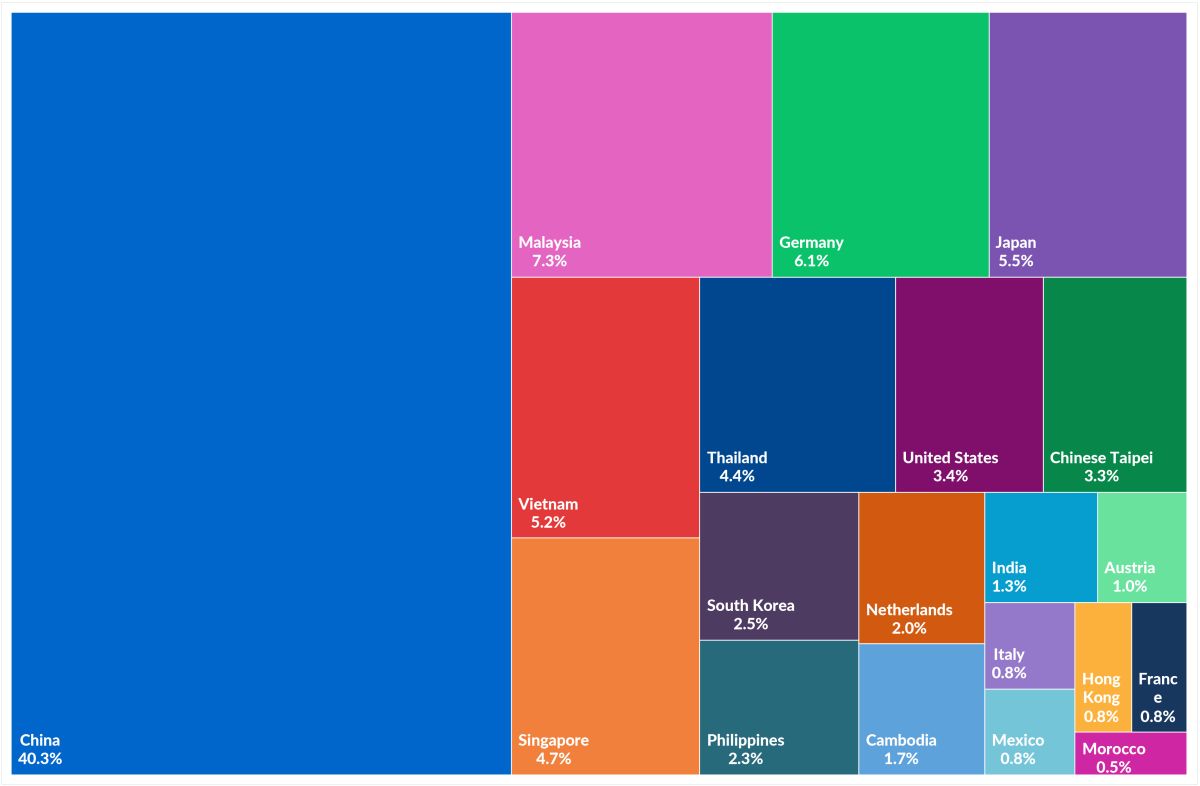

The potential gains of expanding Mexico’s semiconductor industry are recognized in President Sheinbaum’s economic plan—Plan México—which identifies semiconductors as one of its strategic sectors. In 2023, Mexico ranked as the 17th largest exporter of semiconductor devices, capturing about 0.8 percent of global export value, leaving sizable room for growth (Figure 1).

Figure 1. Top 20 Exporters of Semiconductors, by Share of Global Value

Mexico’s long-term competitiveness in this sector will depend on its ability to deliver across four pillars: supply chain, workforce, infrastructure, and entrepreneurship. These pillars—outlined in the National Semiconductor Economic Roadmap—were designed to provide a roadmap to the success of the US’s development of its semiconductor industry.

Supply chain resiliency refers to a country’s ability to access global supplies of materials, equipment, and capacity for assembly, testing, and packaging, while maintaining open access to end markets. Mexico has both the resource base and the trade capacity required to support a robust, globally integrated semiconductor supply chain.

Several critical minerals, along with some noncritical materials such as silicon, are essential to semiconductor production. According to information from S&P Global, Mexico ranks among the top three suppliers of 14 minerals deemed critical by the US Department of Defense. Moreover, its production of these critical minerals has risen in the past five years. Given Mexico’s proximity and strong trade relations with the US, its mineral output can be relatively easily integrated into other critical supply chains.

Mexico’s extensive trade network further strengthens its position. According to Mexico’s Ministry of Commerce, the country has 14 free trade agreements covering 52 countries. This facilitates access to both inputs and end markets, reducing trade barriers and enhancing global integration. For materials not yet mined at scale, Mexico can leverage regional trade relationships, particularly in Latin America, to help close sourcing gaps.

A key constraint for Mexico’s development of resilient supply chains is its existing backlog and restrictions on new mining concessions. According to an article by El Financiero, 391 mining concessions were left on hold under former president Lopez Obrador’s administration. However, under President Sheinbaum, the government has reactivated at least 27 of these projects, sending a positive signal about Mexico’s mining prospects.

Among its core strengths, Mexico’s workforce and growth potential stand out as defining advantages. While talent shortages remain a global bottleneck for the semiconductor industry, Mexico offers a large, underutilized talent pool with significant growth potential. According to the Center for Security and Emerging Technology, 26 percent of Mexico’s graduates come from science, technology, engineering, and mathematics (STEM) fields. Moreover, the number of STEM graduates increased by approximately 30 percent between 2015 and 2020.

According to El Economista, Mexico is projected to have a surplus of 278,000 STEM professionals in the coming years. Gender inclusion presents an additional opportunity. As reported by Mexico’s Competitiveness Institute, women comprise 30 percent of Mexico’s STEM workforce, but their labor force participation remains low. Expanding women’s role in high-skill sectors could further yield significant economic gains.

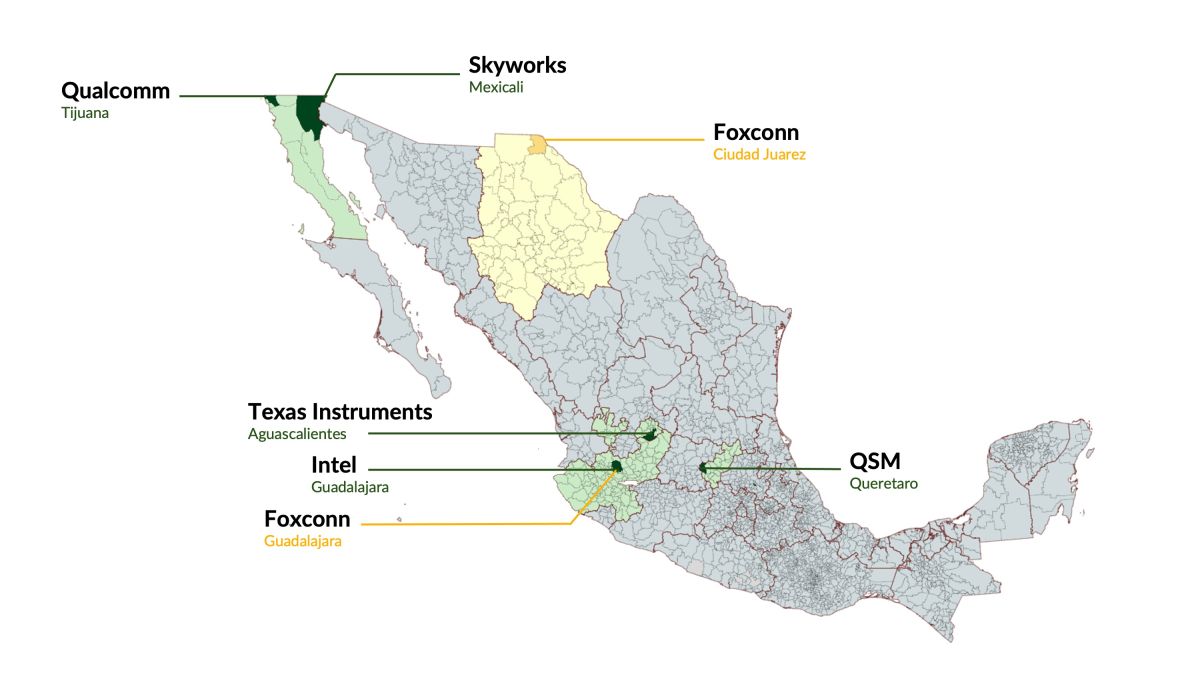

Mexico’s infrastructure reveals both notable strengths and clear opportunities for improvement. According to the International Trade Centre, Mexico is the world’s 16th-largest exporter of electronic integrated circuits. The country’s broad industrial base spans from the northern states of Chihuahua and Baja California to the central regions of Guadalajara and Querétaro (Figure 2). Reliable infrastructure throughout its vast territory is essential to Mexico’s industrial growth, though major challenges remain.

Figure 2. Semiconductor Manufacturing in Mexico

As reported by Mexico Business News, 91 percent of Mexico’s industrial parks experienced power supply disruptions in 2023. Reliable access to electricity, clean water, and advanced logistics is essential for semiconductor manufacturing, particularly if Mexico aims to move into front-end fabrication. These infrastructure needs will demand targeted investment and coordination across federal, state, and private actors.

Mexico’s innovation ecosystem remains underdeveloped and, much like its infrastructure, reflects a need for improved coordination, strategic direction, and sustained investment. Promising research and development efforts, such as the National Polytechnic Institute’s Lagarto microprocessor, and government initiatives like the Kutsari project, show considerable potential. However, greater public and private investment is still needed to scale the industry.

Despite encouraging signals, Mexico has yet to make a concrete investment commitment. Based on the authors’ calculations using Pitchbook data, nearly three-fourths of the capital raised by Mexican companies since 2016 has come from foreign investors, reflecting a strong reliance on foreign capital. In contrast, India and Brazil have committed over US$9 billion and US$4.5 billion to their semiconductor industries, with domestic firms like Tata in India and Zilia in Brazil leading the way, with investments of US$11 billion and US$120 million, respectively. Mexico’s largest announced private domestic investment to date is the $12 million QSM plant planned in Querétaro.

Mexico has signaled its political commitment to strengthen its semiconductor industry. Plan México has laid the groundwork for capacity-building, with an ambitious goal of doubling semiconductor exports by 2030.

The potential upside is substantial. According to the World Bank’s World Integrated Trade Solution, Mexico’s semiconductor imports exceeded US$23.5 billion in 2024, indicating that domestic demand alone could justify large-scale investments. The country’s ability to compete in semiconductor manufacturing depends on its advances in the four pillars outlined above, backed by the decisive execution of President Sheinbaum’s agenda.

Leer en español.