Insights

SHARE

SHARE

Medical care is a large financial burden on many middle- and low-income Americans’ lives. This burden can be so great that the financial impact of obtaining medical care can itself cause meaningful degradation in a patient’s quality of life, a phenomenon referred to as financial toxicity, as explained in JAMA Oncology. For most Americans, health insurance is the primary line of defense against financial toxicity.

Health insurance, like all forms of insurance, does not directly protect against harm. Just as car insurance does not prevent a fender-bender, health insurance does not shield a person from developing an illness or injury. Rather, insurance protects from the financial consequences of harm: repairing a car when it is damaged or paying for medical treatment when a person gets sick.

As discussed in the American Economic Journal: Economic Policy and the Journal of Public Economics, an established causal link exists between gaining health insurance and sizable reductions in adverse financial outcomes such as having debt in collections. There is also causal evidence that those who have their health insurance (specifically Medicaid) taken away have a subsequent increased risk of carrying delinquent debt. The financial protection feature of health insurance is of great policy importance as any policy aimed at health insurance does double duty as a policy impacting household finance.

A recent example of the impact of health insurance on households’ finances is the “Medicaid Unwinding,” or returning to normal Medicaid operations after the ending of some of the rules from the Families First Coronavirus Response Act (FFCRA). The FFCRA temporarily required states to maintain continuous enrollment for those already in a state Medicaid program, meaning that those who had eligibility lapse or who missed re-enrollment would not lose coverage. The Consolidated Appropriations Act, 2023 removed the continuous enrollment rule as of March 31, 2023, and gave states 12 months to return to normal operations.

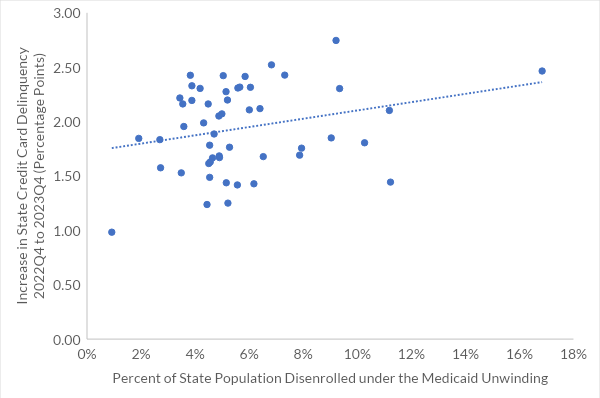

During this time frame, a sizable portion of Medicaid enrollees were disenrolled, according to KFF. The proportion of a state’s total population losing coverage ranged from under 1 percent in Wyoming to over 16 percent in Oklahoma. A correlation between the disenrollment rate and measures of household financial stability can be seen using credit card data from the Federal Reserve: States that had a larger proportion of their population removed from Medicaid during the Medicaid Unwinding also, on average, saw an increase in the likelihood of having delinquent credit card debt during the same time period.

State Medicaid Disenrollment and Increase in Proportion of Credit Cards in Delinquency

Source: Federal Reserve Bank of New York Quarterly Report on Household Debt and Credit (2023), Kaiser Family Foundation Medicaid Enrollment and Unwinding Tracker (2024), US Census Bureau (2023)

The takeaway is clear: Any policy that impacts health insurance coverage needs to be handled with caution. Health insurance and household financial stability are linked, and any policies that change insurance coverage spill over into the economy more broadly via household finance. Policymakers should carefully consider the connection between household financial stability and insurance coverage in their cost-benefit analyses of health insurance policies.

SHARE

Related Content

-

Coverage and Reimbursement Roadmap for Women’s Health Innovation

Women's health has long been underserved by a coverage system built around inadequate research, insufficient billing codes, and payers that have been slow to recognize conditions that affect women exclusively, differentially, or...View Research

LM

LM

-

Advancing Blood-Based Biomarkers for Alzheimer's and Cognitive Care

For the first time in health care's long search for answers on Alzheimer's disease, we have two reasons for hope: simple, accurate diagnostics and approved treatments that slow progression.Read Report

-

Stories from the Field: Uché Blackstock

Q: You recently moderated a panel on the economic case for health equity at the Milken Institute Global Conference. What stood out most to you from the conversation?Read Article -

Milken Institute Statement on HHS-Wide Effort to Strengthen American Leadership in Clinical Trials

Today, Esther Krofah, EVP of Health for the Milken Institute, participated in a roundtable with HHS Secretary Robert F. Kennedy, Jr., and HHS leadership to launch a department-wide effort to strengthen American scientific leadership in...Read StatementImage

Esther Krofah

Executive Vice President, Milken Institute HealthEsther Krofah is the executive vice president of Health at the Milken Institute, leading FasterCures, Public Health, the Future of Aging, and Feeding Change. A recognized expert in health policy, biomedical innovation, and clinical research, Krofah has extensive experience shaping health initiatives that unite diverse stakeholders, foster collaboration, and motivate action toward shared goals. -

Employer Priorities: Advancing Organizational and Employee Health

Employers are uniquely positioned to drive internal and external change and meaningful outcomes for employees, their businesses, and surrounding communities through four key levers captured in the Milken Institute Employer Action Exchange...Read Report

-

Milken Institute, Ann Theodore Foundation Award $600,000 in New Funding to Rising Sarcoidosis Researchers, Invite Applicants for Next Cycle

June 18, 2026 (Washington, DC)—The Milken Institute Science Philanthropy Accelerator for Research and Collaboration (SPARC), in partnership with the Ann Theodore Foundation (ATF), today announced that the Ann Theodore Foundation Learning...Read ArticleImage

Libby Miller

Associate Director, Media Relations, Milken InstituteLibby Miller is an associate director of media relations for the Milken Institute. Based out of the Washington, DC office, she oversees media coverage for the Strategic Philanthropy pillar. -

Access Point: Trends in Clinical Trials Transformation #4

FasterCures’ Access Point: Trends in Clinical Trials Transformation is a quarterly horizon scan examining how emerging trends, organizations, and initiatives are transforming clinical trial access and efficiency.Read Report -

Activating the Food Is Medicine Ecosystem: A Framework for Stakeholder Partnerships

Food Is Medicine (FIM) has reached a critical inflection point. What began as a community-rooted response to unmet nutrition needs has evolved into a nationally recognized strategy for preventing and treating diet-related chronic disease...Read Report CS

CS